Send your good work in the knowledge base is simple. Use the form below

Students, graduate students, young scientists who use the knowledge base in their studies and work will be very grateful to you.

Posted on http://www.allbest.ru/

1 . Calculation of the economic efficiency of the implemented IS

In this thesis project, we will determine the economic efficiency of implementing a system for accounting for clients and resources spent on repair work.

The economic effect of implementing the system can be direct and indirect. Direct - savings in material and labor resources and money obtained as a result of reducing the consumption of basic and auxiliary materials due to the automation of specific types of work. economic monetary repair costs

Indirect - cost savings in the production process, manifested in the final result economic activity companies. Both types are interconnected with each other.

The implementation of any project requires material and financial costs. It is always associated with risk, since it is impossible to say in advance to what extent the project will be commercialized and whether there will be consumers for the new product or service. Therefore, the preliminary assessment stage is an important link in innovation activities. Despite the complexity of the assessment, it is necessary and is a factor that reduces the risk of activity.

To evaluate a project for the degree of its feasibility means assessing the socio-economic efficiency of the project at a stage when there is little reliable information, therefore assessments should be interval: from optimal to pessimistic forecast.

1 . 1 Indirect economic effect

The implementation of a sales automation system will allow:

Ш saving the client in the database;

Ш submission of an application for delivery of goods;

Ш predict the date of purchase of goods

W increase the competitiveness of the company in the market for the services provided.

Since centralized storage of information is used, its reliability and reliability increases, which also cannot but affect the time it takes for the manager to process data on requests; therefore, there is no need to manually compare the data received for processing with real data. Such a reduction in terms will increase the speed of the information circulation process and the responsiveness of employees, which will lead to an increase in labor productivity.

1 . 2 Calculation of direct economic effect

Overall economic efficiency is defined as the ratio of the effect to the capital costs that caused this effect.

It is recommended to compare different investment project options and select the best one using various indicators, which include:

Net present value (NPV) or integral effect;

Profitability index (ID);

Internal discount rate (IRR);

Payback period.

Net present value is the excess of integral results over integral costs. Defined as the sum of current effects for the entire calculation period, reduced to the initial step.

If during the billing period there is no inflationary change in prices or the calculation is made in base prices, then the NPV value for a constant discount rate is calculated using the formula:

where Dt are the results achieved at the t-th calculation step;

Рt - costs incurred at the same step;

b - discount rate;

Дt - Рt - effect achieved at the t-th step.

If the NPV of an investment project is positive, then the project is effective (at a given discount rate), and the issue of its adoption can be considered. The higher the NPV, the more effective the project. If the investment project is implemented with a negative NPV, the investor will suffer losses (the project is ineffective).

The profitability index is the ratio of the sum of the given effects to the amount of capital investment:

The profitability index is constructed from the same elements as the NPV. If the NPV is positive, then ID > 1 and vice versa.

The internal discount rate is the discount rate at which the value of the reduced effects is equal to the reduced capital investment.

IRR is the solution to the equation:

Calculation of the NPV of an investment project shows whether it is effective at a certain given discount rate.

Payback period is the minimum time interval from the start of the project, beyond which the integral effect becomes and subsequently remains non-negative. Those. the payback period is the period measured in months, quarters or years, from which the initial investments and other costs associated with the investment project are covered by the total results of its implementation.

1 . 3 Schedule of main stages in creating the project

The schedule for creating a sales automation system includes the following stages:

1. Pre-project research (planning and analysis of requirements, research and analysis of the existing system, determination of requirements for the created IS);

2. Development of technical specifications;

3. Implementation (development and debugging of a sales automation system, filling the database);

4. Testing (comprehensive debugging of the system);

5. Project implementation (hosting on the provider’s server, staff training);

6. Operation (content management).

The design schedule for a sales automation system, taking into account the duration and costs of each design period, is shown in Table 3.1.

The duration of development and implementation of the software package was 1 month, 20 working days.

Table 3.1 Schedule plan design schedule.

|

Stage |

Duration, in days |

Wage Database developer, rub. |

|

|

Total |

The developer's salary is 9,000 rubles. per month.

Since there are approximately 20 working days in a month, therefore

rub/per day

We will analyze the costs of creating and implementing the system.

Let's determine one-time costs, i.e. those investments that are made once when creating the system. Such costs include costs for technical, system and software.

1 .3.1 Costs for technical support

When developing the task, the following technical means were chosen: PC, global Internet. The organization already has all these technical means and their power is sufficient to provide a solution to the problem.

Therefore, the cost of the selected technical equipment cannot be taken into account when calculating the costs of the technical means necessary to solve the problem.

Thus, the cost of technical support is 0.

1 . 3.2 System costs

When developing the system, it was proposed to use the following system software:

Microsoft Windows Ultimate and 1C 8.3.

One of the main conditions for system development is the obligation to use only licensed software and development tools.

Microsoft Windows Seven Ultimate OS is installed at the Workplace. Since all the system software is already available at the enterprise, the cost of purchasing licensed software products is 0

1 .3 .3 Fixed costs

In addition to one-time implementation costs, fixed costs will inevitably arise during the operation of the system.

Fixed (current) costs include: energy costs, costs of consumables.

Table 3.2 Calculation of electricity for an eight-hour working day

|

Name |

quantity |

kW/hour |

kW per day (approx.) |

kW per month |

|

|

Lighting |

|||||

|

Air conditioner |

|||||

|

Total: |

For individuals 1 kW/h = 3.25

Per month 3.25*208= 676 rubles.

Table 3.3 Calculation of monthly costs for maintaining the system.

Of these: electricity consumption by equipment - 676 rubles.

R post = 676 rub. - fixed monthly expenses.

The operating life of the system will be three years, since technologies are continuously developing and will require an updated approach to creating a sales department automation system. Fixed costs and estimated savings over the operating life (based on the stability of the economic situation for the entire period under consideration) are shown in Table 3.4.

Table 3.4 Fixed costs

|

Period (year) |

||||

|

1 (2014) |

2 (2015) |

3 (2016) |

||

|

Maintenance costs |

||||

|

Total in year |

On this moment, in the absence of an automated system for receiving applications, all information processing by the office operator is carried out manually. These actions take the company manager a total of 4 to 5 hours a day per day, depending on the number of clients that day, this leads to lost profits and loss of potential clients. Knowing the daily wage (on average it is 410 rubles/day), we can calculate that this work costs the company an amount equal to:

rub/per hour

rub/per day

Therefore, the daily payment for this work is 255 rubles/day.

rub/per month

rub/per year

Since it took 20 days to develop the system, these days must be deducted from the annual funds for remuneration of the Database developer.

rub/per year

Since the system is scheduled to be put into operation at the beginning of July, we divide the cost savings for 2014 by half. Then we get a savings of 35,130 rubles.

After commissioning the sales department automation system, it will take the manager approximately 1 hour to process the information.

rub/per day

rub/per month

rub/per year

Labor savings will be:

rub/per year

Also an undeniable convenience for the enterprise is the absence of the need for expensive long-distance negotiations with long-distance clients.

Table 3.5 Current savings

Based on the data from tables 3.4 and 3.5, we will construct a histogram of income and expenses (Fig. 3.1).

Fig.3.1. Company income and expenses

From Fig. 3.1 it is clearly seen that the savings from the implementation of the developed system are several times higher than the costs and the net income increases every year.

1 .4 Economic indicators of the effectiveness of the project being developed

The economic situation in our country is not stable and the inflation rate may change upward, that is, when the money supply depreciates, we will calculate the discount rate taking into account inflation.

b = (refinancing rate - percentage of inflation)

(1+percent inflation)

Table 3.6 One-time costs

|

Name |

Amount, rub. |

|

|

One-time costs |

||

|

Total |

Let's summarize the calculation of indicators in a table.

Table 3.7 Economic indicators of the developed system

|

Periods |

Actual |

1/(1+b)t |

Discounted |

Annualecon. |

NPV with cumulative total |

|||

|

D, rub. |

R, rub. |

D", rub. |

R", rub. |

effect |

||||

|

201 4 |

||||||||

|

2015 |

||||||||

|

2016 |

||||||||

|

Total: |

Based on these data, we calculate the payback period of the system (Fig. 3.2).

Rice. 3.2. System payback period

Analyzing the graph, it is clear that the payback period for the system will occur in the first year of its operation at the enterprise.

1 .5 Conclusion

As a result of the research carried out in this section of the diploma project, it was found that the economic efficiency from the implementation of the developed system will amount to 114,186 rubles over 3 years. Moreover, the system will pay for itself within the first year after its implementation.

Thus, the feasibility of using the developed system lies in the absence of costs when implementing the system and a significant expansion of the client base. Maintenance of the system will not require the recruitment of additional personnel, since this work can be carried out by the office manager, who was previously responsible for processing applications.

Based on the above, we can conclude that the implementation of this system is economically feasible and effective.

2 . Occupational Safety and Health

Occupational safety is the creation of safe and healthy working conditions by various means. The concept of labor protection is distinguished in the broad and narrow sense of the word.

In a narrow concept, labor protection should be understood as ensuring healthy and safe working conditions by all means: legal, economic, medical, organizational and technical, sanitary and hygienic, medical and preventive directly at the workplace. In a broad sense, the term “labor protection” is used to refer to the entire set of labor law norms aimed at the comprehensive protection of all labor rights, that is, the right to work and its payment, to rest, and so on.

2 .1 Legal andregulatory and technical basis

Legislative and legal basis labor protection and environment constitute the relevant laws and regulations adopted by the representative bodies of the Russian Federation, as well as by-laws, decrees of the Government of the Russian Federation, decrees of the President, decrees of local authorities and instructions of specially authorized bodies.

Among the sources of labor law is the Constitution Russian Federation is a fundamental law, an act of supreme legal force. It is a document of direct effect, establishes the basic provisions of the legal system, consolidates the initial principles characteristic of all branches of law, including labor law (Articles 2, 7, 24, 37, 41, 42, 45, 60).

After the Constitution of the Russian Federation, among the labor laws, the most important is the Labor Code of the Russian Federation of February 1, 2002, which establishes state guarantees of labor rights and freedoms of citizens, the creation favorable conditions labor, protection of the rights of workers and employers (No. 116-FZ, 125-FZ, 165-FZ)

ь Law of the Belgorod Region “On Labor Protection” dated March 25, 1999. determines the occupational safety management system in the Belgorod region;

b Federal Law “On the protection of the population and territory from natural and man-made emergencies (1994), which forms the legal basis for organizing work in emergency situations;

ь Federal Law No. 69-FZ “On fire safety»;

b Fire safety rules (PPB 01-03);

b Federal Law No. 123-FZ “Technical Regulations on Fire Safety Requirements”;

b Federal Law No. 384-FZ “Technical Regulations on the Safety of Buildings and Structures”.

b Law “On Environmental Protection”, introduced in January 2002 and aimed at ensuring environmental safety on the territory of the Russian Federation;

b Law “On the sanitary and epidemiological welfare of the population” (1991), establishing criteria for the safety and harmlessness of factors in the human environment;

b Law “On compulsory social insurance against industrial accidents and occupational diseases” dated July 7, 2003 No. 118-FZ establishes the legal, economic and organizational foundations of social insurance;

State regulatory requirements for labor protection in the Russian Federation include the following tasks:

Intersectoral rules on labor protection (IOT R M), intersectoral standard instructions on labor protection (TI R M).

Industry rules on labor protection (POT R O), standard instructions on labor protection (TI R O).

Safety rules (PB), design and safe operation rules (PUBE), safety instructions (IS).

State standards of the labor safety standards system (GOST R SSBT).

Construction norms and rules (SNiP), codes of design and construction rules (SP).

State sanitary and epidemiological rules and regulations (sanitary rules (SP), hygienic standards (GN), sanitary rules and standards (SanPin), sanitary standards(SN)).

SanPiN 2.2.2.542-96 “Hygienic requirements for video display terminals, personal computers and work organization.”

2.2 Organizational arrangements

Occupational safety measures - planned specific activities of the organization aimed at achieving goals in the field of labor protection, determined by the requirements of legislative and other regulatory legal acts, as well as the organization’s policy in the field of labor protection; is an integral part of the occupational safety management system (OSMS), ensures the implementation of occupational safety programs.

The basis of these activities is safety precautions - a system of organizational measures and technical means that prevents the impact of hazardous production factors, which is an integral part of labor protection.

In the process of vehicle maintenance and repair, a number of works are performed, characterized by the complexity of technical operations and the variety of equipment used. Safety conditions when performing all types of work are necessarily specified in the descriptions of the technological process, technological maps and instructions for using the equipment. At the same time, for all types of transport, it is possible to identify areas of work that are similar in the content of technological operations and safety requirements.

Staging on Maintenance and repairs. Maintenance and repairs are carried out in specially designated areas or at specialized enterprises (repair bays). A vehicle sent for maintenance and repair is washed and cleared of dirt, snow, ice, and the remainder of the cargo being transported. Cars are washed and cleaned of dirt using a hose washing method in an open area or mechanically in a room equipped with a washing installation. Car washing takes place in conditions high humidity, dust and gas contamination of the air, the presence of toxic substances in wastewater. This requires compliance with special techniques for performing technological operations and special clothing.

The vehicle is transported to the place where maintenance work is performed by self-propelled vehicle or by towing. Towing is carried out using signals and commands indicating the start of movement, maneuvering and stopping.

Lifting the car. Lifts or lifting structures are used to lift the vehicle. The work is carried out under the supervision of a specially authorized person (engineer, foreman), who monitors compliance with safety regulations and the operation of lifting equipment. When lifting a vehicle, people are not allowed to be in the cabin, on the roof, or below the lifted vehicle. Completion of the lift is accompanied by fixing the lift in the raised position.

Organizational safety measures include:

Instructing and training workers in harmless and safe work practices and methods;

Occupational safety briefing- this component the general process of training employees of the organization, the regularity and quality of which determines the general working climate in the organization.

Experience shows that 60-80% of all accidents and accidents occur for reasons beyond the control of technology and equipment.

Labor safety briefings are carried out with all employees of the enterprise in accordance with GOST 12.0.004-90. Organization of occupational safety training.

Instructions are divided into:

1.introductory;

2.primary at the workplace;

3.repeat;

4. unscheduled;

5.target.

Introductory training on labor protection

Introductory training on occupational safety is carried out with all newly hired workers, regardless of their education, work experience in a given profession or position, with temporary workers, business travelers, students and students arriving for on-the-job training or practice.

Induction training at the enterprise is carried out by a labor protection engineer or a person assigned these responsibilities by order of the enterprise.

At large enterprises, appropriate specialists may be involved in conducting individual sections of induction training.

Introductory training is carried out in a labor protection office or a specially equipped room using modern technical means training and visual aids (posters, full-scale exhibits, models, models, films, filmstrips, videos, etc.).

Initial training at the workplace

Initial briefing at the workplace before the start of production activities is carried out by:

b with all those newly hired at the enterprise, transferred from one division to another;

b with employees performing new work for them, business travelers, temporary workers;

ь with builders performing construction and installation work on the territory of an operating enterprise;

ь with students and students who arrived for industrial training or practice before performing new types of work.

Persons who are not involved in the maintenance, testing, adjustment and repair of equipment, the use of tools, the storage and use of raw materials and materials do not undergo initial training at the workplace.

The list of professions and positions of workers exempt from initial training at the workplace is approved by the head of the organization in agreement with the trade union committee and the labor protection engineer.

Re-briefing

All workers undergo repeated training, with the exception of persons exempt from initial training at the workplace, regardless of qualifications, education, length of service, or the nature of the work performed, at least once every six months.

Enterprises and organizations, in agreement with trade union committees and relevant local government supervisory authorities, may set a longer period (up to 1 year) for repeated training for some categories of workers.

Repeated briefing is carried out individually or with a group of workers servicing the same type of equipment and within a common workplace according to the initial training program at the workplace in full.

Unscheduled briefing

Unscheduled briefing is carried out by:

Upon the introduction of new or revised standards, rules, instructions on labor protection, as well as amendments to them;

When changing the technological process, replacing or upgrading equipment, devices and tools, raw materials, materials and other factors affecting labor safety;

If workers and students violate labor safety requirements, which can lead or have led to injury, accident, explosion or fire, poisoning;

At the request of supervisory authorities;

During breaks in work - for work for which additional (increased) labor safety requirements are imposed by more than 30 calendar days, and for other works - 60 days.

Unscheduled briefing is carried out individually or with a group of workers of the same profession. The scope and content of the briefing is determined in each specific case, depending on the reasons and circumstances that necessitated its implementation.

Targeted briefing

Targeted instruction is carried out when performing one-time work not related to direct responsibilities in the specialty (loading, unloading, cleaning the territory, one-time work outside the enterprise, workshop, etc.); liquidation of consequences of accidents, natural disasters and catastrophes; production of work for which a permit, permit and other documents are issued; conducting excursions at the enterprise, organizing public events with students (excursions, hikes, sports competitions, etc.).

Initial on-the-job, repeated, unscheduled and targeted briefings are carried out by the immediate supervisor of the work (foreman, industrial training instructor, teacher).

On-the-job training ends with a test of knowledge through oral questioning or technical training, as well as a test of acquired skills in safe work practices. The knowledge is checked by the employee who conducted the instruction.

Persons who have demonstrated unsatisfactory knowledge independent work or practical exercises are not allowed and are required to undergo instructions again.

The employee who conducted the briefing makes an entry in the workplace briefing logbook and (or) in a personal card with the obligatory signature of the person being instructed and the person instructing about the conduct of initial briefing at the workplace, repeated, unscheduled, internship and admission to work. When registering an unscheduled briefing, indicate the reason for it.

Targeted briefing with employees carrying out work under a permit, permit, etc. is recorded in the permit or other documentation authorizing the work.

Ш training in the use of protective equipment used on the basis of industrial sanitation and occupational hygiene standards;

Industrial sanitation is defined as a system of organizational measures and technical means that prevent or reduce the impact of harmful production factors on workers.

Occupational health characterized as preventive medicine, studying the conditions and nature of work, their impact on the health and functional state of a person and developing scientific basis and practical measures aimed at preventing the harmful and dangerous effects of factors in the working environment and the labor process on workers.

Ш development and implementation of work and rest regimes when performing operations related to exposure of workers to hazardous or harmful production factors.

2.3 Analysis of hazardous and harmful production factors

A person is exposed to hazards in his work activities. This activity takes place in a space called the work environment. In production conditions, humans are mainly affected by man-made, i.e. associated with technology, hazards that are commonly called hazardous and harmful production factors.

Hazardous production factor is a production factor, the impact of which on a worker under certain conditions leads to injury or other sudden sharp deterioration in health.

Injury -- this is damage to body tissues and disruption of its functions by external influences. An injury is the result of an industrial accident, which is understood as a case of exposure to a hazardous production factor on a worker while performing his job duties or tasks of a work manager.

Harmful production factor is a production factor whose impact on a worker under certain conditions leads to illness or reduced ability to work.

There is often no clear boundary between dangerous and harmful production factors.

Diseases arising under the influence of harmful production factors are called occupational.

To hazardous production factors should include, for example:

b electric current of a certain strength;

b hot bodies;

b the possibility of the worker himself or various parts and objects falling from a height;

b equipment operating under pressure above atmospheric, etc.

To harmful production factors relate:

* unfavorable meteorological conditions;

* dustiness and gas contamination of the air environment;

* exposure to noise, infra- and ultrasound, vibration;

* presence of electromagnetic fields, laser and ionizing radiation, etc.

2 .3.1 Hazards

? Fire danger

Fire is an uncontrolled combustion outside a special fireplace, causing material damage. Large fires often take the form of a natural disaster and are accompanied by accidents to people. Fires are especially dangerous in places where flammable and combustible liquids and gases are stored.

Eliminating the causes of fires is one of the the most important conditions ensuring fire safety at service stations. The enterprise should promptly organize fire safety briefings and classes on fire safety standards. On the territory, in production, administrative, warehouse and auxiliary premises, it is necessary to establish a strict fire safety regime. Special smoking areas must be designated and equipped. Metal boxes with lids are provided for used cleaning material. For the storage of flammable and combustible substances, locations are determined and permissible quantities of their one-time storage are established.

The territory of the ATP must be systematically cleared of industrial waste; the territory of the designed site must be equipped with primary fire extinguishing means.

Fire safety must comply with: the requirements of GOST 12.1.004-85, building codes and regulations

? Electrical hazard

Dangerous and harmful effects on people of electric current, electric arc and electromagnetic fields manifest themselves in the form of electrical injuries and occupational diseases.

The degree of dangerous and harmful effects on a person from electric current, electric arc and electromagnetic fields depends on:

Type and magnitude of voltage and current;

Frequencies of electric current;

Current paths through the human body;

Duration of exposure to electric current or electromagnetic field on the human body;

Environmental conditions.

Standards for permissible touch currents and voltages in electrical installations must be established in accordance with the maximum permissible levels of human exposure to touch currents and voltages and approved in the prescribed manner.

Electrical safety requirements when exposed to electric fields of industrial frequency according to GOST 12.1.002-84, when exposed to electromagnetic fields of radio frequencies according to GOST 12.1.006-84.

Electrical safety must be ensured:

Design of electrical installations;

Technical methods and means of protection;

Organizational and technical measures.

Electrical installations and their parts must be designed in such a way that workers are not exposed to dangerous and harmful effects of electric current and electromagnetic fields, and comply with electrical safety requirements.

Electrical safety requirements (rules and regulations) for the design and installation of electrical installations must be established in the standards of the Occupational Safety Standards System, as well as in the standards and technical conditions for electrical products.

Technical methods and means of protection that ensure electrical safety must be installed taking into account:

Rated voltage, type and frequency of electrical installation current;

Method of power supply (from a stationary network, from an autonomous power supply);

Neutral (midpoint) mode of the electrical power supply (isolated, grounded neutral);

Type of execution (stationary, mobile, portable);

Environmental conditions;

Particularly dangerous premises;

High-risk premises;

Premises without increased danger;

On open air;

Possibility of relieving voltage from live parts on which or near which work must be carried out;

The nature of possible human touch to the elements of the current circuit:

Ш single-phase (single-pole) touch,

Ш two-phase (two-pole) touch,

Ш touching metal non-current-carrying parts that are energized;

Possibility of approaching live parts that are energized at a distance less than permissible or getting into the zone of current spreading;

Types of work: installation, adjustment, testing, operation of electrical installations carried out in the area where electrical installations are located, including in the area air lines power transmission

Safety requirements for the operation of electrical installations in production must be established by regulatory and technical documentation on labor protection, approved in the prescribed manner.

Safety requirements for using household electrical installations must be contained in the manufacturer's operating instructions attached to them.

To ensure protection against accidental contact with live parts, the following methods and means must be used:

Protective shells;

Safety barriers (temporary or permanent);

Safe location of live parts;

Insulation of live parts (working, additional, reinforced, double);

Isolation of the workplace;

Low voltage;

Safety shutdown;

Warning alarm, lockout, safety signs.

To provide protection against injury electric shock When touching metal non-current-carrying parts that may become live as a result of insulation damage, use the following methods:

Protective grounding;

Zeroing;

Potential leveling;

Protective wire system;

Safety shutdown;

Insulation of non-current-carrying parts;

Electrical network separation;

Low voltage;

Insulation control;

Compensation of ground fault currents;

Individual protection means.

Technical methods and means are used separately or in combination with each other so that optimal protection is ensured.

Requirements for technical methods and means of protection must be established in standards and technical specifications.

Persons who have undergone instruction and training must be allowed to work in electrical installations safe methods labor, testing knowledge of safety rules and instructions in accordance with the position held in relation to the work performed with the assignment of the appropriate safety qualification group and not having medical contraindications.

To ensure the safety of work in existing electrical installations, the following organizational measures must be taken:

Appointment of persons responsible for the organization and safety of work;

Drawing up a work order or order for work;

Granting permission to carry out work;

Organization of supervision of work;

Registration of the end of work, breaks in work, transfers to other workplaces;

Establishment of rational work and rest schedules.

Specific lists of work that must be performed according to the order or order should be established in industry regulatory documentation.

To ensure the safety of work in electrical installations, the following should be done:

Disconnecting the installation (part of the installation) from the power source;

Checking for lack of voltage;

Mechanical locking of switching device drives, removing fuses, disconnecting the ends of power lines and other measures to eliminate the possibility of erroneous supply of voltage to the place of work;

Grounding of disconnected live parts (application of portable grounding conductors, switching on of grounding knives);

Fencing the workplace or live parts that remain energized, which can be touched or approached at an unacceptable distance during work.

When carrying out work involving voltage relief in or near existing electrical installations:

Disconnecting the installation (part of the installation) from the power supply;

Mechanical locking of the drives of disconnected switching devices, removing fuses, disconnecting the ends of the supply lines and other measures to ensure that it is impossible to erroneously supply voltage to the place of work;

Installation of safety signs and fencing of live parts that remain energized, which during operation can be touched or approached at an unacceptable distance;

Applying groundings (switching on grounding blades or applying portable groundings);

Fencing the workplace and installing mandatory safety signs.

When carrying out work on live parts that are energized:

performance of work simultaneously by at least two persons, using electrical protective equipment, ensuring the safe location of working and used mechanisms and devices.

2 .3.2 Harmful factors

· Microclimate.

From a scientific point of view, microclimate is a complex of physical factors of the internal environment of premises that influences the body’s heat exchange and human health. Microclimatic indicators include temperature, humidity and air speed, the temperature of the surfaces of enclosing structures, objects, equipment, as well as some of their derivatives: the vertical and horizontal air temperature gradient of the room, the intensity of thermal radiation from internal surfaces.

If all these parameters are normal, then a person will not experience any sensations of discomfort; he will not feel hot, cold, or stuffiness. Comfortable microclimatic conditions are a combination of microclimate indicator values that, with prolonged exposure to a person, provide a normal thermal state of the body with minimal stress on the thermoregulation mechanisms and a feeling of comfort for at least 80% of people in the room. However, despite its apparent simplicity and clarity, microclimate violations are the most common among all violations of sanitary and hygienic standards.

The following are considered comfortable working conditions:

Air temperature in the workplace, C:

Indoors during the warm period; 18-22

Indoors during the cold period;20-22

Outdoors during warm periods; 18-22

Outdoors during cold periods; 7-10

Relative air humidity, %40-54

Air speed, m/s: less than 0.2

Toxic substances (multiplicity of maximum permissible concentration) less than 0.8

Industrial dust (multiplicity of maximum permissible maximum) less than 0.8

The required air condition in the work area can be ensured by performing certain measures, the main ones of which include:

Mechanization and automation of production processes, remote control by them;

The use of technological processes and equipment that prevent the formation of harmful substances or their entry into the work area;

To normalize the air, ventilation, both natural and artificial, is used. Air conditioning ensures automatic maintenance of microclimate parameters within the required limits throughout all seasons of the year, cleaning the air from dust and harmful substances.

· Air dustiness

Air dust content should not exceed 19.6 mg/m3. One specialist working in a car service must have a room volume of 150 m 3 with an area of 70 m 2 (excluding passages and equipment). During a working day, it is necessary to ensure air exchange in a room with a volume of 150-250 m3, moisture removal of 350-500 g and heat of 50 kJ for each kilogram of body weight of the worker.

? Negative effects of noise

Noise is a chaotic combination of sounds of different frequency and strength that adversely affect the human body, interfering with its production work and rest.

Noise and vibration are among the common environmental factors that adversely affect the human body. People who work in high-noise environments complain of fatigue, headache, insomnia. A person's visual and hearing acuity decreases, blood pressure, attention weakens, memory deteriorates. Vibration, in turn, affects the central nervous system, on the vestibular apparatus, has a negative effect on equipment. All this leads to a significant decrease in labor productivity, an increase in the number of errors in work, and a decrease in the service life of equipment.

In rooms where workers are located, the noise level should not exceed 82 dB. At workplaces in rooms housing noisy units, the noise level should not exceed 98 dB.

Reducing vibration and noise created at workplaces by internal sources, as well as noise penetrating from outside, is carried out by the following methods: by reducing noise at the source, equipment, devices, instruments are installed on special foundations and shock-absorbing pads. Perforated slabs, panels and other materials of similar purposes are used as sound-absorbing material, as well as thick cotton fabric, which is used to drape the ceiling and walls. Suspended acoustic ceilings can also be used.

? Insufficient lighting

Natural lighting in production, auxiliary and household premises must comply with the requirements of current building codes and regulations. Premises for storing vehicles, warehouses, as well as other premises, permanent stay workers that are not required may be without natural light.

Windows facing the sunny side must be equipped with devices that provide protection from direct sunlight.

It is not allowed to block windows and other light openings with materials, equipment, etc.

The light openings of the upper lanterns should be glazed with reinforced glass or metal mesh should be suspended under the lantern to protect against possible glass falling out.

Cleaning the glazing of light openings and lanterns from contamination should be carried out regularly, in case of significant contamination - at least 4 times a year, and in case of minor contamination - at least 2 times a year.

To ensure safety when cleaning the glazing of light openings, you should use special devices (step ladders, scaffolding, etc.).

Premises and workplaces must be provided with artificial lighting sufficient for the safe performance of work, stay and movement of people in accordance with the requirements of current building codes and regulations.

Cleaning of lamps must be carried out within the time limits specified in the current building codes and rules.

The design and operation of the artificial lighting system must comply with the requirements of current regulations.

Luminaires must be located so that they can be safely serviced.

For power supply of general lighting lamps in premises, a voltage of no higher than 220 V is used, as a rule. In premises without increased danger, the specified voltage is allowed for all stationary lamps, regardless of the height of their installation.

In rooms with increased danger and especially dangerous when installing lamps with a voltage of 220 V for general lighting with incandescent lamps and gas-discharge lamps at a height of less than 2.5 m, it is necessary to use lamps whose design excludes the possibility of access to the lamp without the use of a tool. Electrical wiring supplied to the lamp must be in metal pipes, metal hoses or protective shells. Cables and unprotected electrical wires can only be used to power lamps with incandescent lamps with a voltage not exceeding 50 V.

Lamps with fluorescent lamps with a voltage of 127 - 220 V may be installed at a height of less than 2.5 m from the floor, provided that their live parts are not accessible to accidental touches.

For local lighting of workplaces, lamps with non-translucent reflectors should be used. The design of local lighting fixtures must provide for the possibility of changing the direction of light.

To power local stationary lighting fixtures, the voltage must be used: in rooms without increased danger - no higher than 220 V, and in rooms with increased danger and especially dangerous - no higher than 50 V.

12 - 50 V sockets must be different from

plug sockets with a voltage of 127 - 220 V, and plugs 12 - 50 V should not fit into sockets 127 - 220 V.

When using fluorescent and gas-discharge lamps for general and local lighting, measures must be taken to eliminate the stroboscopic effect. In damp, especially damp, hot and chemically active environments, the use of fluorescent lamps for local lighting is allowed only in fittings special design. Illumination of inspection ditches with lamps with a voltage of 127 - 220 V is permitted subject to the following conditions:

All electrical wiring must be internal (hidden), with reliable electrical and waterproofing;

Lighting equipment and switches must have electrical and waterproofing;

Lamps should be covered with glass or protected with a protective grille;

Metal housings of lamps must be grounded (zeroed).

Emergency lighting must provide the necessary illumination for the continuation of work or the safe exit of people from the premises in the event of a sudden shutdown of the working lighting.

Emergency lighting luminaires must be connected to an electrical network independent of the working lighting and switch on automatically when the working lighting is suddenly turned off.

In premises for storing vehicles operating on CNG, as well as in premises for their maintenance, repair and inspection technical condition Emergency lighting must be provided in accordance with the requirements of current regulations.

In these premises, the power supply for emergency ventilation, emergency lighting, as well as the gas environment control system must be provided according to the first category of power supply reliability.

To power portable lamps in high-risk and especially dangerous areas, it is necessary to use a voltage not exceeding 50 V.

In the presence of particularly unfavorable conditions, when the danger of electric shock is aggravated by cramped conditions, uncomfortable position of the worker, contact with grounded (zero) surfaces (work in boilers, containers, etc.), a voltage of no higher than 12 V is used to power portable lamps.

In explosive areas, explosion-proof lamps should be used, and in fire hazardous areas, lamps in a moisture-proof and dust-proof, closed version should be used.

The room for the acetylene generator must have external electric lighting through tightly closed transom windows.

2 .3.3 Emergency

Extremely high flows negative impacts create emergency situations (ES). In accordance with GOST R.22.0.02-94, an emergency situation is a condition in which, as a result of the occurrence of a source of emergency, a facility, a certain territory or water area is disrupted normal conditions life and activity of people, there is a threat to their life and health, damage is caused to the property of the population, the economy and the environment.

The source of an emergency situation is understood as a dangerous natural phenomenon, accident or dangerous man-made incident.

Experience shows that an emergency situation at industrial facilities goes through five conventional typical phases in its development:

1. Accumulation of deviations from the normal state or process; the phase is relatively long in time, which makes it possible to take measures to change or stop the production process and significantly reduces the likelihood of an accident and subsequent emergency situations;

2. The initiating event phase or the “emergency” phase. The phase is significantly short in time, although in some cases there may still be a real opportunity to either prevent an accident or reduce the scale of the emergency;

3. The process of an emergency event, during which there is a direct impact on people, objects and the natural environment of primary damaging factors; in the event of an industrial accident during this period, energy is released, which can be destructive;

4. Phase of action of residual and secondary damaging factors;

5. Emergency response phase.

Let's consider a possible emergency- fire during welding work in the area of the post for plumbing and mechanical works.

1. When using a welding machine, a spark hits flammable objects and substances (upholstery, plastic, gasoline, kerosene, etc.). It is possible to prevent this by pre-repair disassembling the upholstery, placing a damp cloth in places where sparks are expected to hit, and having fire extinguishing agents on hand.

2. Car fire. It is still possible to extinguish the fire using fire extinguishing agents.

3. From a burning car, the fire spreads to the walls and ceilings of the building, thereby endangering the lives of workers and visitors to the car service center.

4. Possible human losses, burns and poisoning, building collapse, loss of equipment.

5. Call the fire brigade, fire extinguishing, immediate health care those in need.

The consequences of a car fire can be material for the car owner, as well as possible poisoning from combustion products and burns.

2 .4 Calculation part

Ventilation is a device for forced regulation of air exchange in a room. The ventilation system is an essential item and is designed to ensure the necessary cleanliness, temperature, humidity and air mobility in the room. In the absence of ventilation in a closed room, people's well-being worsens, drowsiness and headaches appear.

For many production premises, air purity, temperature and humidity play a significant role in production. Therefore, it is necessary to create forced air exchange in the room, due to the design of ventilation equipment, air conditioners, filters, heaters, etc. The ventilation system allows you to organize such climatic conditions under which the safety of materials, objects, and equipment occurs.

For calculation we apply the following methodology:

The size of the car service room where our employee sits is calculated using the formula:

Where V pom- volume of working space (m 3);

a - room width (m);

b- length (m);

h- height (m).

The volume of air is determined based on the heat balance equation:

Where V vent- volume of air required for exchange;

Q excess - excess heat (W);

C = 1000- specific thermal conductivity of air (J/kgK);

Y = 1.2- air density ().

The temperature of the exhaust air is determined by the formula:

Where t = 1-5°C- excess t at 1m of room height;

t r.m. = 25 °C- temperature in the workplace;

h= 3.5 m - room height;

t coming= 18 degrees.

Excess heat from electrical equipment and lighting:

E- coefficient of electricity loss for heat removal ( E=0.55 for lighting);

...Similar documents

Studying the essence of analysis of the use of material resources. In-production reserves and saving of material resources. Assessing the quality of logistics plans, the need for material resources, and the efficiency of their use.

course work, added 10/07/2010

Simple, normative, incremental and order-based cost accounting methods. Analysis of production costs, profits and profitability of the enterprise. Assessment of indicators of the use of material resources. Finding internal production reserves for their savings.

course work, added 02/24/2016

Labor resources as a socio-economic category. Formation of labor resources at the enterprise. Key indicators of efficiency in the use of labor resources. Increasing the efficiency of using labor resources using the example of OJSC TMTP.

thesis, added 04/09/2015

Analysis of fixed assets and labor resources: labor productivity, capital intensity, capital ratio, capital productivity; depreciation of fixed assets. Use of labor resources in the enterprise. Analysis financial results: costs, profit, profitability.

practical work, added 04/25/2013

Essence, criteria and assessment of economic efficiency of production. Dependence of production efficiency on production economy mode. Directions for increasing production efficiency. Factors that hinder the effective operation of the organization.

course work, added 11/15/2013

The concept of material resources. The importance of saving material resources. Methodology for analyzing the use of material resources. Analysis of the efficiency of use of material resources at JSC Daldizel. Recommendations for optimizing their use.

course work, added 10/13/2003

A system of indicators for assessing the efficiency of using the organization's resources. Organizational and economic characteristics of RUE "Gomselmash". Analysis of the use of fixed production assets. Carrying out measures to save enterprise resources.

course work, added 09/27/2013

The importance and role of labor resources in increasing the efficiency of production. Analysis of the efficiency of using labor resources at OJSC Dalsvyaz. Main measures to improve the efficiency of using the enterprise's labor resources.

course work, added 06/17/2010

Kinds automated systems enterprise management: Axapta, SAP R/3 and Baan. Calculation of costs for creating the "HTControl" system. Calculation of total cost savings, capital investments and expenses. Annual economic effect from the implementation of the development.

course work, added 02/25/2013

Organizational and economic characteristics of Aktiv-plus LLC. Indicators of the solvency of the enterprise. Direct, indirect, coefficient analysis methods cash flows. Ways to improve enterprise security in cash and their use.

Skripov D.K., Ph.D.

OJSC VTB Bank, Deputy Head of Service in DIT

graduate of MBA group CIO-32A

RANEPA School of IT Management under the President of the Russian Federation

Gribanov S.P.

School of IT Management RANEPA under the President of the Russian Federation

When implementing any information system In a large enterprise, the question always arises about the feasibility of the costs associated with its value. It is very important to assess as fully as possible all planned costs, including the cost of licenses, the cost of services for implementation / modification of the system and the cost of support. Although for most projects it is impossible to reliably translate into monetary form the image and other intangible assessments caused by the implementation of this information system, detailed analysis direct and indirect costs and income allows us to draw a reliable conclusion about the need for its implementation.

To assess the result of implementing an information system, economic efficiency can be defined as the difference between the total income from using the information system and the costs of the information system during its life cycle. But before implementing the system, future income cannot be determined accurately; it can only be estimated based on the practice of implementing similar systems. Therefore, at first they usually talk only about qualitative forecast indicators.

Like many large companies, JSC VTB Bank simultaneously implements a large number of projects that influence each other and are not related. Projects, as steps in the process of implementing a long-term IT strategy, in addition to compliance with the bank’s business strategy, are also assessed by the economic efficiency of the information systems being implemented or modified. Especially due to the fact that decisions on the implementation of projects pass through a long chain of people in the extensive structure of the Bank, and are ultimately accepted collectively by the Committee on Banking Information Technologies, a unified, transparent method for representatives of various departments is needed, allowing one to compare the cost of projects and take responsibility decision to implement them.

OJSC VTB Bank is the parent enterprise of the VTB Group. The state's share in the capital of VTB Bank is 60.9%. VTB Group is an international financial group providing a wide range of banking services. VTB Group consists of VTB Bank and its subsidiaries credit and financial institutions. Subsidiary credit organizations carry out banking operations, subsidiaries financial institutions provide services in the securities market, insurance services or other financial services. VTB Group today consists of more than 30 companies in more than 20 countries. The Group's companies employ more than 90,000 people.

In accordance with the development strategy of the VTB Banking Group, the main direction of activity is increasing shareholder value.

Modern banking activities are impossible without credit institutions using advanced information technologies, which allows not only to improve the quality of banking services provided, but also to expand their list. As practice shows, the use modern technologies credit institutions ensures a significant increase in the efficiency of their activities.

The IT Strategy is an integral part of the overall development strategy of the VTB Group and determines the directions of IT development in the VTB Group.

The main goals of the IT strategy are:

- optimization of VTB Group IT costs;

- improving the quality and reliability of IT services;

- providing additional competitive advantages for business through information technology;

- IT preparation for the possible merger of the Group's large Russian banks.

The VTB Group’s construction of a corporate governance system is aimed at maximizing the use of its advantages, increasing its share in target markets, increasing efficiency indicators and increasing the level of capitalization of the VTB Group.

Thus, in the competitive conditions of the modern market, which require constant addition and/or change of banking products, a fast, effective and manageable system of knowledge transfer between Bank employees is very important. The challenges of knowledge transfer are further magnified for the banking group as a whole.

Current system distance learning The Group is fragmented and does not currently meet the needs of the Group, as it does not reflect the matrix management system and existing Global business lines.

The Group lacks rapid and standardized training across Global Business Lines, Support Lines and Product Verticals.

Thus, it is necessary to create an operational system for the implementation and dissemination of knowledge across business lines, support lines and product verticals (including new procedures, policies, reporting standards, service standards and others). A unified centralized training system for VTB Group companies will allow:

- ensure control over the quality of training in the Group, including by filling courses and providing feedback

- create a common group system for knowledge management and exchange of best practices

- to ensure a significant reduction in costs for full-time training (not only functional, but also skill-based) without loss of quality, as well as for supporting existing portals in different companies of the group, purchasing similar and interchangeable electronic courses.

Currently, distance learning systems are used autonomously in almost half of the Group's companies. However, some portals contain less than ten courses and are practically not used.

VTB Group's unified training portal will allow you to:

- create a unified training space for all VTB Group companies

- create a platform for knowledge exchange between Group companies

- implement PR functions at the Group level

- provide all Group employees with access to courses on personal effectiveness, management, working with software, etc.

The introduction of automated distance learning systems provides cost savings on employee training from 30% to 80% (see, for example), mainly due to a reduction in travel expenses for employees and/or trainers. Also remote systems training allow tens of thousands of workers to be trained in short time(for example, familiarization with a new banking product in two weeks).

The existing training system used at VTB Bank does not meet business requirements. Processes for implementing system changes do not satisfy users and need to be redesigned.

Methods for assessing economic efficiency

Currently, the literature mainly considers two approaches for assessing the cost-effectiveness of implementing an information system. The first is to use static estimates, without taking into account the time value of money. The main indicator is Total Cost of Ownership(Total Cost of Ownership, TCO). The specificity of the indicator is that it takes into account only the expenditure part of the project. There is no universal mechanism for calculating the indicator; direct and indirect costs are taken into account different types depending on the object being assessed. First, the Gartner Group in 1987, and then Interpose, later acquired by the Gartner Group, back in 1994, proposed an approach using comparisons with similar average costs depending on the profile of the enterprise, which practically turned this method into an industry standard for estimating the cost of ownership of an information system.

ITIL Service Strategy () identifies six main cost characteristics, divided into three groups, such that any type of cost can be attributed to exactly one element of each of these three groups:

- Basic or operational

- Direct and indirect

- Fixed and variable expenses.

Only fixed costs can be amortized. Depreciation is necessary because information systems can cost significant sums and be designed for many years of use, and of course their cost turns out to be much higher than the income for the first year of use. In accordance with the Tax Code of the Russian Federation, electronic computer equipment belongs to the second group of depreciable fixed assets with a depreciation period of 2 to 3 years.

The main articles for which the assessment takes place ():

- equipment costs (Equipment Cost Unit, ECU);

- software costs (Software Cost Unit, SCU);

- personnel costs (Organization Cost Unit, OCU);

- accommodation costs (Accommodation Cost Unit, ACU);

- transfer costs (Transfer Cost Unit, TCU) associated with goods and services provided by other departments, i.e. internal settlements between departments of the organization;

- Cost Accounting (CA) costs associated with the IT financial management process.

The next indicator for analyzing system implementation is Return on investment(Return On Investment, ROI). This ratio shows the return on capital invested in the project:

,

(1)

where is the invested funds, is the value at the end of the period, is profit. It is also called return on equity.

The coefficient is convenient to use to answer the question of how effective the project is (). Also closely related to it is the project’s payback period; this is the period of time needed for the project to reach break-even.

Another convenient indicator is Economic added value(Economic Value Added, EVA). Economic value added is the difference between a company's net operating profit and all costs incurred:

, (2)

where is net operating profit after taxes,

– weighted average cost of capital, – invested funds.

The complexity of calculating the indicator is manifested in the assessment of the parameters used.

If the return on investment is written in the form  ,

,

then the indicator of economic added value is determined as follows:

.

That is, any investment creates added value only if its after-tax return exceeds the weighted average cost of capital.

When it is not possible to explicitly estimate the profit received in the future, it is estimated by reducing labor intensity or eliminating the need to perform operations due to the implementation of an information system. Estimates of the corresponding savings are multiplied by the average wage and increased by the amount of taxes (insurance premiums) and the cost of the workplace.

The key disadvantage of calculating TCO for assessing economic efficiency is the lack of accounting for the revenue side of the project, as well as changes in the cost of money for long-term projects. Therefore, further we will use methods that take into account the concept of discounted cash flows with various modifications. Thus, for any cash flow we will determine its value reduced to a given point in time.

The main indicator for this concept is the indicator Net present value(Net Present Value, NPV):  (3)

(3)

where net present value is the invested funds, r –

discount rate, – total cash flow in k-th period, including financial, investment and operating flows. Typically, cash flows are recorded over periods of one year.

Another commonly used indicator is Internal rate of return(Internal Rate of Return, IRR). IRR is the rate at which the Net Present Value becomes 0.

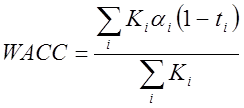

To calculate the Net Present Value, as well as the value with which the Internal Rate of Return can be compared, it is necessary to estimate the discount rate as accurately as possible. The discount rate depends on the mechanisms for obtaining money for the project, as well as the ability to reliably invest money. For a more accurate assessment or a longer period of consideration of the economics of the project, the Weighted Average Cost of Capital (WACC) indicator can be used. WeightedAverageCost ofCapital) , (4)

, (4)

where is the price of each source in the total cost of capital,

– tax rate, positive if expenses can be excluded from the tax base, – rate of the corresponding source.

In practice, when actually assessing the effectiveness of investment projects for making a responsible investment decision, the above indicators are not calculated separately, but all together, since each of them has both positive and negative properties.

Thus, the following combination of methods is optimal from the point of view of completeness and minimization of costs for conducting an assessment:

- determination of the cost part of the project using the TCO method

- determining the effects of implementing the system. This work may consist of several components:

- forecasting the effect of implementation based on the results achieved in previously successfully implemented similar projects in companies belonging to the same sector of the economy;

- forecasting the effect based on assessments of business customers.

- taking into account the risks associated with the implementation project.

The existence of a corporate culture in a company often makes it difficult (and usually quite significant) to introduce new technologies, including new information systems. Therefore, it is imperative to take into account corporate characteristics.

Example of choosing an information system

In accordance with the IT strategy, the structure of the Bank, and taking into account the analysis of the market for automated training systems, we will consider in detail the implementation of the Bank’s requirements in the software products WebTutor by Websoft and Competentum Shareknowledge by Competentum. Widespread best of breed training systems of foreign companies, such as Saba or SAP R3, in addition to the severity of technical modifications, have the cost of licenses alone, which significantly exceeds the full cost of implementation and modification of the Russian systems in question.

The weight of the scoring table criteria (see Fig. 1) was chosen based on the experience of implementing similar projects in the Bank. The main criterion is cost (25%), since the project must be cost-effective. The next most important criterion (20%), which means greatest influence– this is the compliance of the product as is with the stated business requirements. Since any modification carries some risk and also takes time, then of course the system with the least required modification has an advantage. The high weight of non-functional requirements (15%) is caused by the requirements of controlling internal departments, for example, such as the mandatory provision of access rights to information systems through a role structure. Modifications of information systems in order to meet such requirements, if they were not initially provided for during the design, usually require large time and material costs.

Rice. 1 . Evaluation of automated training systems

The labor costs for the implementation project based on the software product Competentum Shareknowledge and Microsoft Sharepoint Server were estimated by Microsoft, the work received was converted into cost taking into account the market prices of large automation companies. In accordance with the obtained figures, we calculate the financial indicators described above (calculation is in millions of rubles):

TCO = 15

ROI =19.6 / 15 – 1 = 30%

PI = 18.5 / 15 = 123%

NPV = 3.5

EVA = 4.6 – 0.035*3*15 = 3.03

IRR is about 10%.

The main contribution to cost reduction is made by the expense item for transferring training standards to the Group's subsidiaries under the Change Management program. These costs include conducting training for selected local providers and their certification according to the program and built-in elements, taking into account the average cost of payment to each of the providers, travel expenses, and quality control of trainings, that is, a trip to the subsidiary bank of the provider-holder of the program and/or Service employees corporate training for support and quality control, as well as the actual conduct of training by local providers in the subsidiary bank.

In the process of assessing economic efficiency, the following conclusions can be drawn:

Corporate management systems

One of the problems in determining the effectiveness of system-wide and office software(PO) is the choice of assessment methodology. In the classical literature devoted to the issue of efficiency assessment, it is calculated using the formula:

Costs - the total costs of acquisition, installation and configuration, maintenance and support, as well as costs associated with equipment downtime during maintenance or troubleshooting.

Effect - the effect achieved when implementing software. However, due to the specifics of using general system and office software, it is difficult to determine the direct effect of their implementation (in time or financial terms). As a result, the task of choosing an assessment method arises, the entire set of which can be divided into:

- 1. Costly methods. Evaluation is made not on the basis of measuring the final product or result, but on the basis of the resources or effort expended.

- 2. Methods for assessing direct results. The methodology evaluates a direct measurable result, for example, a reduction in the cost of ownership, an increase in system functionality, a reduction in labor costs, or the emergence of a by-product of the main labor production.

- 3. Methods based on assessing the ideality of the process. Such techniques are based on static or dynamic comparative algorithms. The object of the system under consideration is selected as the base indicator, then the information system with the best cost per unit of output indicators for the industry is considered ideal. Approaches based on comparison with an alternative solution are also popular.

- 4. Qualimetric approaches. Such methods take a comprehensive look at the information system, organize its measurement and process the results obtained using statistical, sociological and/or expert methods.

Cost-based valuation methods.

Boiler method. The method is based on determining the ratio of the volume of investments in software, including implementation and maintenance, with the size of the enterprise and the directions of its business. Often this ratio is set in the form of the maximum allowable amount of investment in relation to the company’s annual turnover, for example, no more than 1% for small companies and no more than 3% for large ones.

Function point method. This method is used to approximate the cost of creating and implementing an information system (IS) depending on user requirements. Each such requirement is rated both on a scale of difficulty (easy, medium and difficult) and on a scale of importance to the user. Requirements are represented as a vector (function point) in a multidimensional space. Further, in accordance with the “compactness” hypothesis, it is assumed that the closer the functional points of projects are to each other in the requirements space, the more similar their parameters, including efficiency, are. Accordingly, in the database of previously implemented projects there is one whose functional point is closest to the designed IS, and it is assumed that their effectiveness is as close as possible.

Total cost of ownership (TCO - total cost of ownership). This method involves a quantitative assessment of the implementation and maintenance of software, calculated using the formula:

where: - assessment of integrated costs for the project at the moment; E - discount rate, reflecting the temporary nature of financial resources; - discounted amount of actually incurred integral costs at the moment; T - period of the system life cycle; - assessment of the integral costs of the project in period t.

The TCO model allows you to understand the structure of costs associated with IP and opens up broad prospects for reducing them, also helps to identify current problems, and provides constant feedback in cost management.

Methods for assessing direct results.

Consumer index. This method involves assessing the results of software implementation in the form of a set of indices that reflect positive changes in the company’s work (increased income, reduced costs, increased turnover, increased customer base, etc.).

Applied information economics (AIE - applied information economics) - the methodology is similar to the consumer index, but unlike it, it also involves the assessment of various subjective indicators, for example, ease of working with the system, customer satisfaction, etc.

Economic value sourced (EVS - source of economic value). It is an assessment of how much benefit software brings to a company when using it, assessed by four indicators: increased revenue, increased productivity, reduced product release time, and reduced risks.

Economic value added (EVA - economic value added). This technique involves defining the effect as the actual profit from using the software, which is equal to net operating profit minus the cost of capital. In relation to IT projects, EVA means that:

- · when using capital in IT projects, it is necessary to take into account its cost; it must be paid for in the same way as for the labor of employees;

- · IT professionals are expected to sell their services to other departments at market rates.

This allows IT to be viewed as a profit center rather than a cost center, while clearly showing how revenues are growing.

Techniques based on process ideality.

These methods are based on comparing the results of software implementation with existing good (ideal) examples. And it is assumed that the closer we get to these examples, the higher the efficiency of the implemented software. These methods include:

Industry average results. In this case, the effectiveness of software implementation is assessed in comparison with average industry results. These results are commonly reported in public publications and marketing materials.

Gartner Measurement. According to this method, effectiveness determines how well a given information system meets the needs of the user. In this case, the focus is not only on the internal capabilities of the system, but also on the subjective opinion of clients and objective data of various implementation options. To do this, qualitatively evaluate such criteria as the time spent setting up the system, implemented functionality, average number of users per server, average and peak number of transactions per unit of time, cost of one transaction, average and peak system response time, training methods used, cost of information system infrastructure per user. Based on such a study, a specific implementation option is evaluated, and it is compared with others (previously implemented). And based on the analysis, recommendations are made on improving the operation of the information system, selecting the optimal software configuration, the most effective training methods for a given client, and integrating information systems with other customer systems.

Return of investment (ROI - return on investment). The essence of the methodology is to select for the company standard project, optimal in terms of return on investment in software.

Qualimetric methods.

Total economic impact (TEI - total economic impact model). The TCO model is used as the cost component of this method, and the effect is calculated based on the following factors:

- · Advantages. Comparison of labor organization options existing and in the predicted information system (as it was - as it will be). Evaluating the differences and comparing the results with the project goals allows you to determine the advantages or disadvantages of the new information system.

- · Flexibility. The flexibility of an information system is assessed in terms of its expandability, as well as its adaptability to new conditions. One of the guarantees of flexibility is the use of standardized and unified solutions, as well as a well-thought-out information system architecture.

- · Risk. Implies the likelihood of financial losses when investing in IT.

Balanced scorecard (BSC - balanced scorecard). This is a system of strategic management of an organization based on measuring and assessing its effectiveness through the use of a comprehensive function that includes a set of indicators that take into account all aspects of the company’s activities (financial, marketing, etc.). These indicators usually include:

- · Critical Factors of Success (CFS) - strategic indicators: finances, customers, internal business processes, training and growth;

- · key performance indicators (KPI), including the achieved results of the company’s activities.

The composition and number of balanced indicators are determined based on the specifics of each company.

Choosing a method for assessing general system and office software

When choosing a method for assessing the effectiveness of general system and office software, the following factors must be taken into account:

- · assessment of both the effect and cost components of efficiency; the ability to determine the effect in relation to system-wide and office software; (the ability to evaluate financial and time indicators, such as labor productivity, reduction in product costs, etc.)

- · the ability to determine indicators without conducting an in-depth survey of the organization’s business processes; this survey is very costly and labor-intensive. And, as a rule, it is only necessary for specialized software;

- · universality of the methodology - determined by the universality of the parameters and the strength of their influence (when changed) on the calculation algorithm.

Table 1. Results of the possibility of using various methods

|

Effect and cost assessment |

Determining the effect for system-wide and office software |

The need for an in-depth examination of the organization |

Versatility |

|

|

Boiler method |

doesn't count |

not required |

universal |

|

|

Function point method |

effect, costs |

applicable |

not required |

not universal |

|

doesn't count |

not required |

universal |

||

|

Consumer Index |

not applicable |

required |

not universal |

|

|

applicable |

not required |

universal |

||

|

not applicable |

required |

not universal |

||

|

effect, costs |

applicable |

required |

universal |

|

|

Industry average results |

not applicable |

not required |

universal |